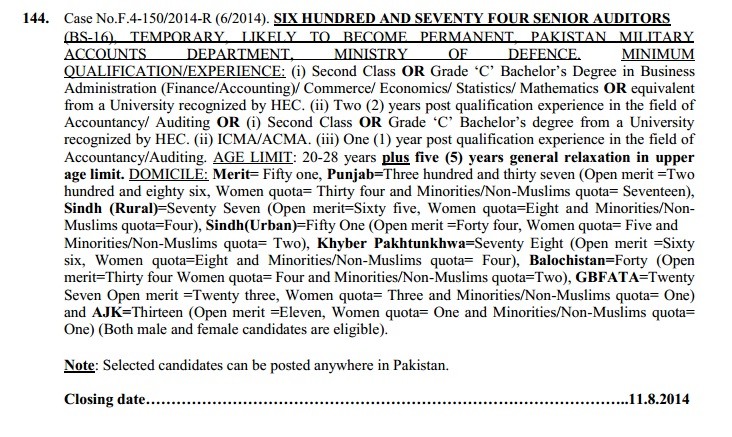

Federal Public Service Commission has announced 674 Vacancies of Senior Auditors BPS-16 in Pakistan Military Accounts Department. Closing date for these vacancies is 11th August 2014. These vacancies are temporary that are likely to be permanent.

Age limit is 20 to 28 years plus five years as general age relaxation. The selected candidates can be posted anywhere all over Pakistan. Minimum qualification and quota has been mentioned on the advertisement. For further details and apply online visit Federal Public Service Commission website.

247 Vacancies in Pakistan Railways (PR)")

Result?????????????

Any one knw about the result..? when they will declare the result..,and how they will declare?

Can you plz tell the accurate date for written test???

Dear Mr. SK, test ki dates to NTS/FPSC ki site per hi ayain gi.

Salam Shumaila,

What will be the expected result date and time span for the procedure. One of my friend told me as per new circular of FPSC they have to complete recruitment process within 60 “Sixty” Days from the date of advertisement. Is it true? Waiting for your reply. Thanks

Dear Naveed mujhay confirm nahin hay.

Allah bless u shumila..gud effort

Thanks Dear Babar

FPSC Senior Auditors Test Preparation Basic Accounting Terms and Questions for Test and Interviews

Share capital: The sum total of the nominal value of the shares of a company is called share capital.

102. Funds flow statement: It is the statement deals with the financial resources for running business activities. It explains how the funds obtained and how they used.

103. Sources of funds: There are two sources of funds internal sources and external sources. Internal source: Funds from operations is the only internal sources of funds and some important points add to it they do not result in the outflow of funds

(a) Depreciation on fixed assets

(b) Preliminary expenses or goodwill written off, Loss on sale of fixed assets Deduct the following items, as they do not increase the funds:

Profit on sale of fixed assets, profit on revaluation Of fixed assets

External sources: (a) Funds from long-term loans

(b)Sale of fixed assets

(c) Funds from increase in share capital

104. Application of funds: (a) Purchase of fixed assets (b) Payment of dividend (c)Payment of tax liability (d) Payment of fixed liability

105. ICD (Inter corporate deposits): Companies can borrow funds for a short period. For example 6 months or less from another company which have surplus liquidity? Such deposits made by one company in another company are called ICD.

106. Certificate of deposits: The CD is a document of title similar to a fixed deposit receipt issued by banks there is no prescribed interest rate on such CDs it is based on the prevailing market conditions.

107. Public deposits: It is very important source of short term and medium term finance. The company can accept PD from members of the public and shareholders. It has the maturity period of 6 months to 3 years.

108. Euro issues: The euro issues means that the issue is listed on a European stock Exchange. The subscription can come from any part of the world except India.

109. GDR (Global depository receipts): A depository receipt is basically a negotiable certificate, dominated in us dollars that represents a non-US company publicly traded in local currency equity shares.

110. ADR (American depository receipts): Depository receipts issued by a company in the USA are known as ADRs. Such receipts are to be issued in accordance with the provisions stipulated by the securities Exchange commission (SEC) of USA like SEBI in India.

111. Commercial banks: Commercial banks extend foreign currency loans for international operations, just like rupee loans. The banks also provided overdraft.

112. Development banks: It offers long-term and medium term loans including foreign currency loans

113. International agencies: International agencies like the IFC,IBRD,ADB,IMF etc. provide indirect assistance for obtaining foreign currency.

114. Seed capital assistance: The seed capital assistance scheme is desired by the IDBI for professionally or technically qualified entrepreneurs and persons possessing relevantexperience and skills and entrepreneur traits.

115. Unsecured loans: It constitutes a significant part of long-term finance available to an enterprise.

116. Cash flow statement: It is a statement depicting change in cash position from one period to another.

117. Sources of cash:

Internal sources

(a)Depreciation

(b)Amortization

(c)Loss on sale of fixed assets

(d)Gains from sale of fixed assets

(e) Creation of reserves

External sources-

(a)Issue of new shares

(b)Raising long term loans

(c)Short-term borrowings

(d)Sale of fixed assets, investments

118. Application of cash:

(a) Purchase of fixed assets

(b) Payment of long-term loans

(c) Decrease in deferred payment liabilities

(d) Payment of tax, dividend

(e) Decrease in unsecured loans and deposits

119. Budget: It is a detailed plan of operations for some specific future period. It is an estimate prepared in advance of the period to which it applies.

120. Budgetary control: It is the system of management control and accounting in which all operations are forecasted and so for as possible planned ahead, and the actual results compared with the forecasted and planned ones.

121. Cash budget: It is a summary statement of firm’s expected cash inflow and outflow over a specified time period.

122. Master budget: A summary of budget schedules in capsule form made for the purpose of presenting in one report the highlights of the budget forecast.

123. Fixed budget: It is a budget, which is designed to remain unchanged irrespective of the level of activity actually attained.

124. Zero- base- budgeting: It is a management tool which provides a systematic method for evaluating all operations and programmes, current of new allows for budget reductions and expansions in a rational inner and allows reallocation of source from low to high priority programs.

125. Goodwill: The present value of firm’s anticipated excess earnings.

126. BRS: It is a statement reconciling the balance as shown by the bank pass book and balance shown by the cash book.

127. Objective of BRS: The objective of preparing such a statement is to know the causes of difference between the two balances and pass necessary correcting or adjusting entries in the books of the firm.

128. Responsibilities of accounting: It is a system of control by delegating and locating the Responsibilities for costs.

129. Profit centre: A centre whose performance is measured in terms of both the expense incurs and revenue it earns.

130. Cost centre: A location, person or item of equipment for which cost may be ascertained and used for the purpose of cost control.

131. Cost: The amount of expenditure incurred on to a given thing.

132. Cost accounting: It is thus concerned with recording, classifying, and summarizing costs for determination of costs of products or services planning, controlling and reducing such costs and furnishing of information management for decision making.

133. Elements of cost:

(A) Material

(B) Labour

(C) Expenses

(D) Overheads

134. Components of total costs: (A) Prime cost (B) Factory cost

(C)Total cost of production (D) Total c0st

135. Prime cost: It consists of direct material direct labour and direct expenses. It is also known as basic or first or flat cost.

136. Factory cost: It comprises prime cost, in addition factory overheads which include cost of indirect material indirect labour and indirect expenses incurred in factory. This cost is also known as works cost or production cost or manufacturing cost.

137. Cost of production: In office and administration overheads are added to factory cost, office cost is arrived at.

138. Total cost: Selling and distribution overheads are added to total cost of production to get the total cost or cost of sales.

139. Cost unit: A unit of quantity of a product, service or time in relation to which costs may be ascertained or expressed.

140.Methods of costing: (A)Job costing (B)Contract costing (C)Process costing (D)Operation costing (E)Operating costing (F)Unit costing (G)Batch costing.

141. Techniques of costing: (a) marginal costing (b) direct costing (c) absorption costing (d) uniform costing.

142. Standard costing: standard costing is a system under which the cost of the product is determined in advance on certain predetermined standards.

143. Marginal costing: it is a technique of costing in which allocation of expenditure to production is restricted to those expenses which arise as a result of production, i.e., materials, labour, direct expenses and variable overheads.

144. Derivative: derivative is product whose value is derived from the value of one or more basic variables of underlying asset.

145. Forwards: a forward contract is customized contracts between two entities were settlement takes place on a specific date in the future at today’s pre agreed price.

146. Futures: A future contract is an agreement between two parties to buy or sell an asset at a certain time in the future at a certain price. Future contracts are standardized exchange traded contracts.

147. Options: An option gives the holder of the option the right to do something. The option holder option may exercise or not.

148. Call option: A call option gives the holder the right but not the obligation to buy an asset by a certain date for a certain price.

149. Put option: A put option gives the holder the right but not obligation to sell an asset by a certain date for a certain price.

150. Option price: Option price is the price which the option buyer pays to the option seller. It is also referred to as the option premium.

151. Expiration date: The date which is specified in the option contract is called expiration date.

152. European option: It is the option at exercised only on expiration date itself.

153. Basis: Basis means future price minus spot price.

154. Cost of carry: The relation between future prices and spot prices can be summarized in terms of what is known as cost of carry.

155. Initial margin: The amount that must be deposited in the margin a/c at the time of first entered into future contract is known as initial margin.

156 Maintenance margin: This is somewhat lower than initial margin.

157. Mark to market: In future market, at the end of the each trading day, the margin a/c is adjusted to reflect the investors’ gains or loss depending upon the futures selling price. This is called mark to market.

158. Baskets: basket options are options on portfolio of underlying asset.

159. Swaps: swaps are private agreements between two parties to exchange cash flows in the future according to a pre agreed formula.

160. Impact cost: Impact cost is cost it is measure of liquidity of the market. It reflects the costs faced when actually trading in index.

161. Hedging: Hedging means minimize the risk.

162. Capital market: Capital market is the market it deals with the long term investment funds. It consists of two markets 1.primary market 2.secondary market.

163. Primary market: Those companies which are issuing new shares in this market. It is also called new issue market.

164. Secondary market: Secondary market is the market where shares buying and selling. In India secondary market is called stock exchange.

165. Arbitrage: It means purchase and sale of securities in different markets in order to profit from price discrepancies. In other words arbitrage is a way of reducing risk of loss caused by price fluctuations of securities held in a portfolio.

166. Meaning of ratio: Ratios are relationships expressed in mathematical terms between figures which are connected with each other in same manner.

167. Activity ratio: It is a measure of the level of activity attained over a period.

168. Mutual fund: A mutual fund is a pool of money, collected from investors, and is invested according to certain investment objectives.

169. Characteristics of mutual fund: Ownership of the MF is in the hands of the of the investors MF managed by investment professionals The value of portfolio is updated every day

170. Advantage of MF to investors: Portfolio diversification Professional management Reduction in risk Reduction of transaction casts Liquidity Convenience and flexibility

171. Net asset value: the value of one unit of investment is called as the Net Asset Value

172. Open-ended fund: open ended funds means investors can buy and sell units of fund, at NAV related prices at any time, directly from the fund this is called open ended fund.

173. Close ended funds: close ended funds means it is open for sale to investors for a specific period, after which further sales are closed. Any further transaction for buying the units or repurchasing them, happen, in the secondary markets.

174. Dividend option: investors who choose a dividend on their investments, will receive dividends from the MF, as when such dividends are declared.

175. Growth option: investors who do not require periodic income distributions can be choose the growth option.

176. Equity funds: equity funds are those that invest pre-dominantly in equity shares of company.

177. Types of equity funds: Simple equity funds Primary market funds Sectoral funds Index funds

178. Sectoral funds: Sectoral funds choose to invest in one or more chosen sectors of the equity markets.

179. Index funds: The fund manager takes a view on companies that are expected to perform well, and invests in these companies

180. Debt funds: the debt funds are those that are pre-dominantly invest in debt securities.

181. Liquid funds: the debt funds invest only in instruments with maturities less than one year.

182. Gilt funds: gilt funds invests only in securities that are issued by the GOVT. and therefore does not carry any credit risk.

183. Balanced funds: Funds that invest both in debt and equity markets are called balanced funds.

184. Sponsor: sponsor is the promoter of the MF and appoints trustees, custodians and the AMC with prior approval of SEBI.

185. Trustee: Trustee is responsible to the investors in the MF and appoint the AMC for managing the investment portfolio.

186. AMC: the AMC describes Asset Management Company; it is the business face of the MF, as it manages all the affairs of the MF.

187. R & T Agents: the R&T agents are responsible for the investor servicing functions, as they maintain the records of investors in MF.

188. Custodians: Custodians are responsible for the securities held in the mutual fund’s portfolio.

189. Scheme takes over: if an existing MF scheme is taken over by another AMC, it is called as scheme take over.

190. Meaning of load: Load is the factor that is applied to the NAV of a scheme to arrive at the price.

192. Market capitalization: market capitalization means number of shares issued multiplied with market price per share.

193. Price earnings ratio: The ratio between the share price and the post tax earnings of company is called as price earnings ratio.

194. Dividend yield: The dividend paid out by the company, is usually a percentage of the face value of a share.

195. Market risk: It refers to the risk which the investor is exposed to as a result of adverse movements in the interest rates. It also referred to as the interest rate risk.

196. Re-investment risk: It the risk which an investor has to face as a result of a fall in the interest rates at the time of reinvesting the interest income flows from the fixed income security.

197. Call risk: Call risk is associated with bonds have an embedded call option in them. This option hives the issuer the right to call back the bonds prior to maturity.

198. Credit risk: Credit risk refers to the probability that a borrower could default on a commitment to repay debt or band loans

199. Inflation risk: Inflation risk reflects the changes in the purchasing power of the cash flows resulting from the fixed income security.

200. Liquid risk: It is also called market risk, it refers to the ease with which bonds could be traded in the market.

Kya test ise me se ayega?

dear madam test 3 months ke lie postpone hogae he kia?

Dear Junaid, I have not heard about this news.

Tests will start from 19 oct 2014

fpsc senior auditor jobs 2014 Last Date Apply August 21-2014 in pakistan military accounts department in pakistan ka return test date Kab ha.

Dear Sanaullah just keep visiting FPSC Thanks

dear book by ilmi publishers in the only book which is according to the syllabus of FPSC. All other books are crap. Stay away from them.

Dear dogra brothers ki book me buht sare questions and problems hn,kya ye problems test me ayngn ya just diffinitions ayngn?

Dear Ambreen main nain kabhi bhi NTS ka test nahin dia. I think the test is on the basis of selection of answers.

hr ek MCQ k lye 1 min dya jaega aur problem solve krne me atleast 6 7 min lgte hn is k bawajood b problems de skte hn kya??

ek aur sawal tha apse kya general knowledge k questions askte hn?

Dear Ambreen, yes. aa saktay hain.

thank u so much dear

madam g.k ae ge fir tu paper out of syllabud hojaega

Will you tell me the test center and timing of test??

Dear Ambreen these details will be available at FPSC website.

Madan passing marks in fpsc exam and is pipfa advantage or not,thank you

Dear Junaid, Mujhay confirm nahin hay.

Any book? Pipfa is an advantage or not?

And also guide for books for preparation madam i will be thanx ful and expected test date,thank you

Dear Junaid, In mine opinion “Dogar Brothers” books on this topic are best. Thanks

when will be the written test ???

Dear Faryal, You should visit the site the FPSC for the written test dates.

How can we apply online where is online form for Pakistan Military accounts? Plz help me for registeration?

Dear Raja Azhar, just visit the website of FPSC for online apply.

Dear share the procdure aftr applying. N regard auditor exam which materials of stdy is proper to qulify well the exam.

Dear Faheem, I think there will be a book of Dogar Brothers on this topic Thanks

Dear sir can the tist of senior editor should be online

Dear M Waheed, mujhay confirm nahin hay.

Dear Shumaila,

Can you please share the maximum age limit for the female candidate to apply for this post? I am of 35, can I apply?

Regards

Dear Tahseen Khan here not mentioned the age limit for the females. However you can try to send your application.

hy dear can i apply for the senior auditor ..i did b,com i have no experirnce.,plz guid me.

Dear Abid aap sirf without experience certificate try ker saktay hain.

HI, SHUMAILA U R DOING GREAT WORK, GOD BLESS U, MAY I ASK WHAT IS THE FEE FOR POST ON SENIOR AUDITOR PLZ.

REGARDS.

Welcome dear Amir Shahzad, The fee for these posts is Rs. 300/-

Madam i applied for s/auditor i recvd condirmation mail from fpsc but i did not print out my slip from fpsc so may i be able to give screening test,Thank you and i am waiting for your reply

Dear Junaid I could not understand ur question. Plz in details Thanks

Madam mene confrmtn mail agae he per jo print out nikalna tha wo nahe nikala mene ab date close hogae wo nahe nikal raha wo print out zarori tu nahe tha na aur admit card tu aege na ya yehe tha jo print out kar ke nikalina tha

Dear Junaid, aap FPSC kay office phone ker kay confirm ker lain. Mujhay confirm nahin hay. Thanks

mujy koi achi book ya web bata dan jis sa men senior auditor k test ki tayari kar sakon

Dear Numan, I think Dogra Brothers Books in this regard are better.