Last Updated on March 21, 2026 by Galaxy World

Here I am sharing the Brief on Income Tax (Amendment) Ordinance 2018 submitted by Mr. Muhammad Husnain. If any amendment/correction required please mention the same in the comments so that there may be correction done.

BRIEF ON INCOME TAX (AMENDMENT) ORDINANCE 2018

Recently, Income Tax (Amendment) Ordinance 2018 has been issued wherein certain amendments in Income Tax Ordinance 2001, have been made.

One amendment is of particular importance and has gained popularity among employees of the government i.e. New Income Tax Slabs with effect from

1st July 2018.

You may also like: Non Filing of Income Tax Returns

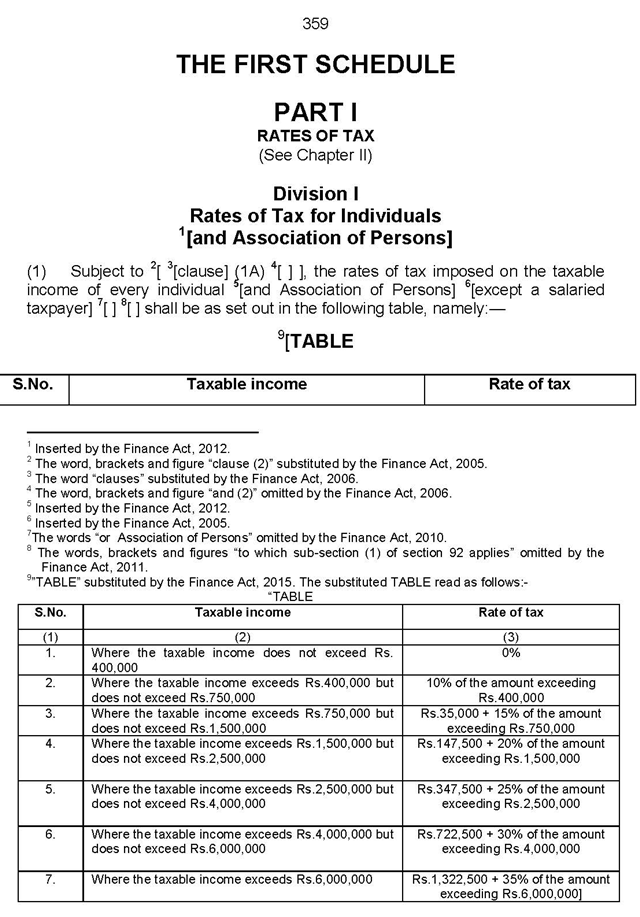

Previously, Income Tax was deducted as per following table:

| S. No. | Taxable Income | Rate of tax |

| 1 | Where the taxable income does not exceed Rs.400,000 | 0% |

| 2 | Where the taxable income exceeds Rs.400,000 but does not exceed Rs.500,000 | 2% of the amount exceeding Rs.400,000 |

| 3 | Where the taxable income exceeds Rs.500,000 but does not exceed Rs.750,000 | Rs.2,000+5% of the amount exceeding Rs.500,000 |

| 4 | Where the taxable income exceeds Rs.750,000 but does not exceed Rs.1,400,000 | Rs.14,500+10% of the amount exceeding Rs.750,000 |

| 5 | Where the taxable income exceeds Rs.1,400,000 but does not exceed Rs.1,500,000 | Rs.79,500+12.5% of the amount exceeding Rs.1,400,000 |

| 6 | Where the taxable income exceeds Rs.1,500,000 but does not exceed Rs.1,800,000 | Rs.92,000+15% of the amount exceeding Rs.1,500,000 |

| 7 | Where the taxable income exceeds Rs.1,800,000 but does not exceed Rs.2,500,000 | Rs.137,000+17.5% of the amount exceeding Rs.1,800,000 |

| 8 | Where the taxable income exceeds Rs.2,500,000 but does not exceed Rs.3,000,000 | Rs.259,500+20% of the amount exceeding Rs.2,500,000 |

| 9 | Where the taxable income exceeds Rs.3,000,000 but does not exceed Rs.3,500,000 | Rs.359,500+22.5% of the amount exceeding Rs.3,000,000 |

| 10 | Where the taxable income exceeds Rs.3,500,000 but does not exceed Rs.4,000,000 | Rs.472,000+25% of the amount exceeding Rs.3,500,000 |

| 11 | Where the taxable income exceeds Rs.4,000,000 but does not exceed Rs.7,000,000 | Rs.597,000+27.5% of the amount exceeding Rs.4,000,000 |

| 12 | Where the taxable income exceeds Rs.7,000,000 | Rs.1,422,000+30% of the amount exceeding Rs.7,000,000 |

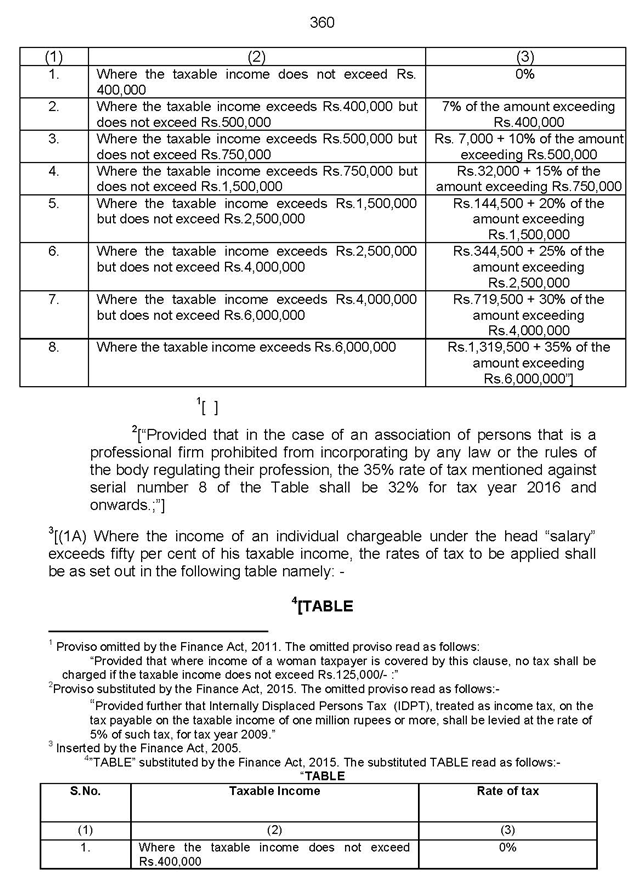

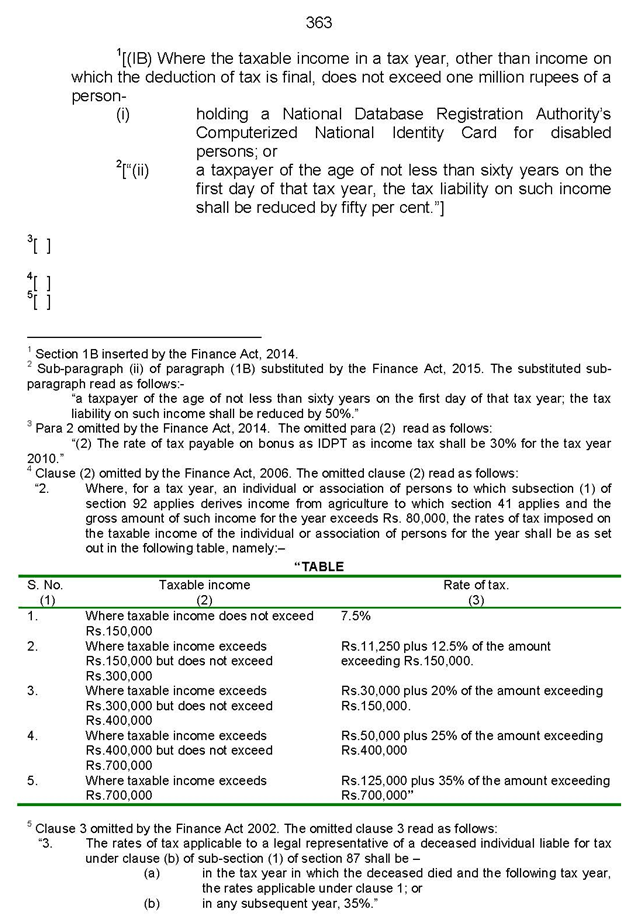

This Tax Rate is listed in SCHEDULE-I, PART-I, DIVISION-I of Income Tax Ordinance 2001 (Amended upto 30-06-2017), placed below:

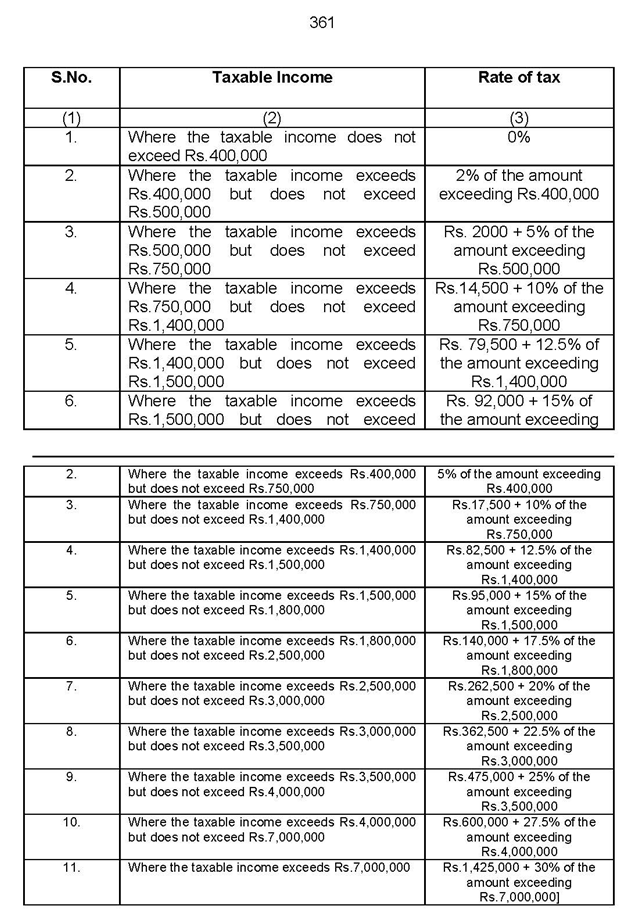

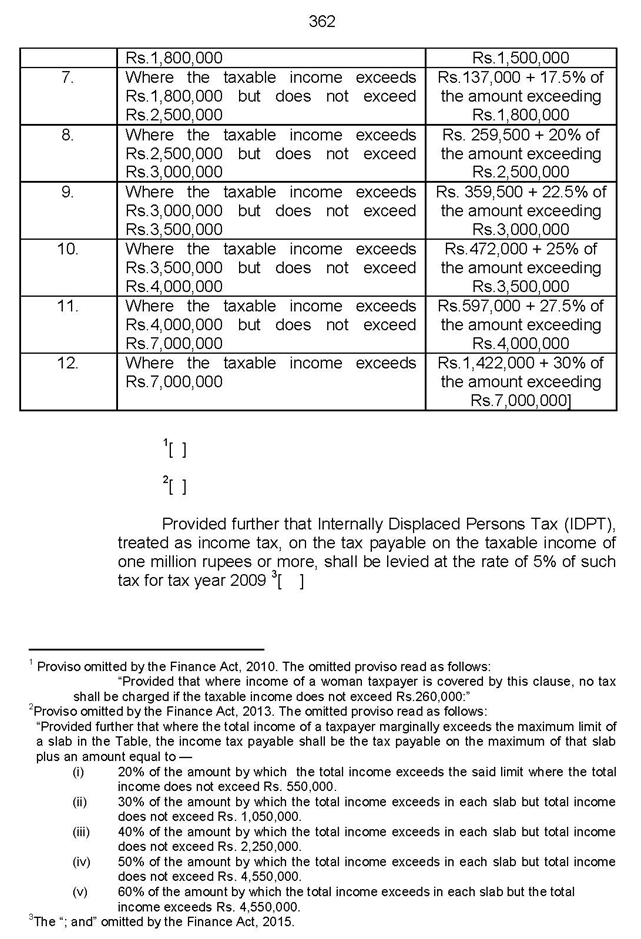

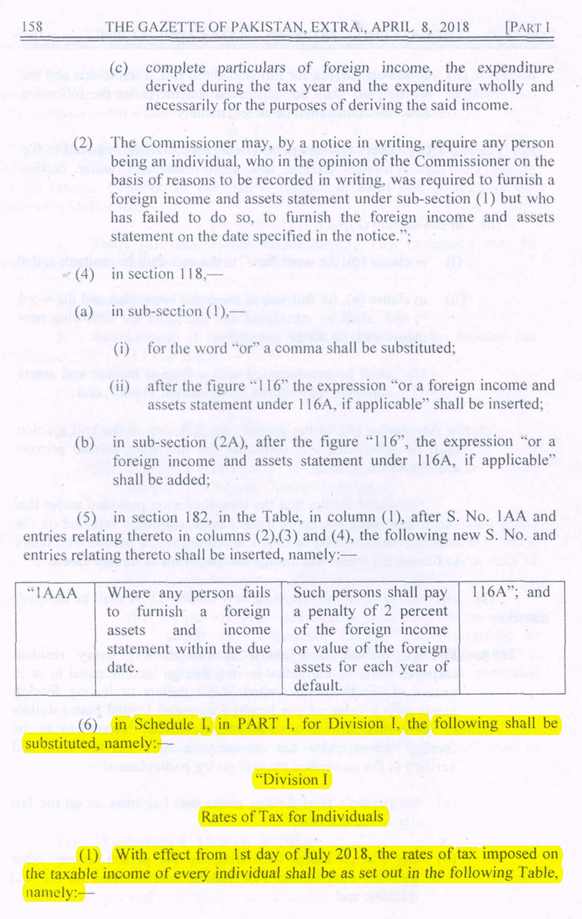

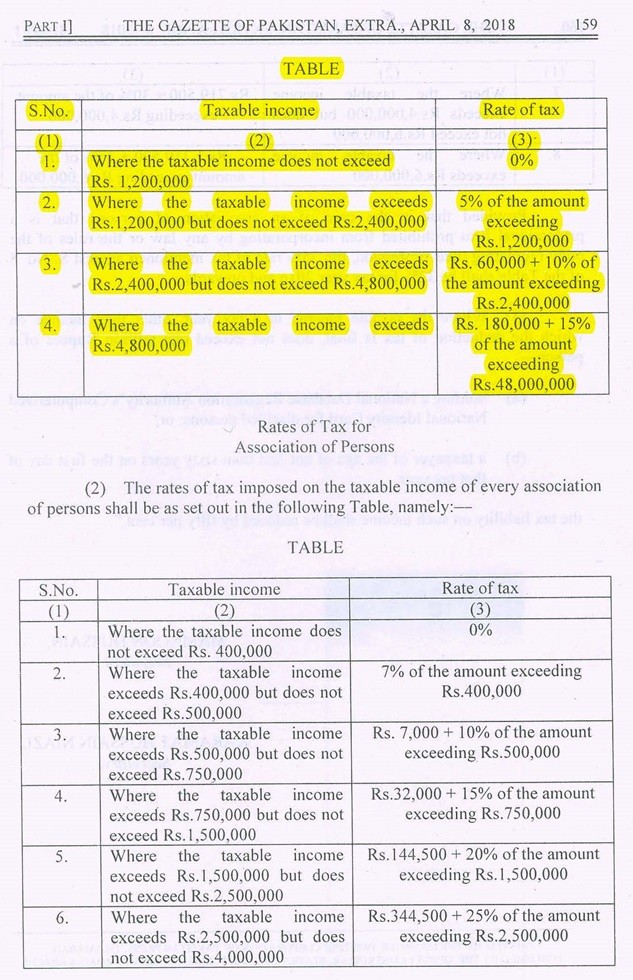

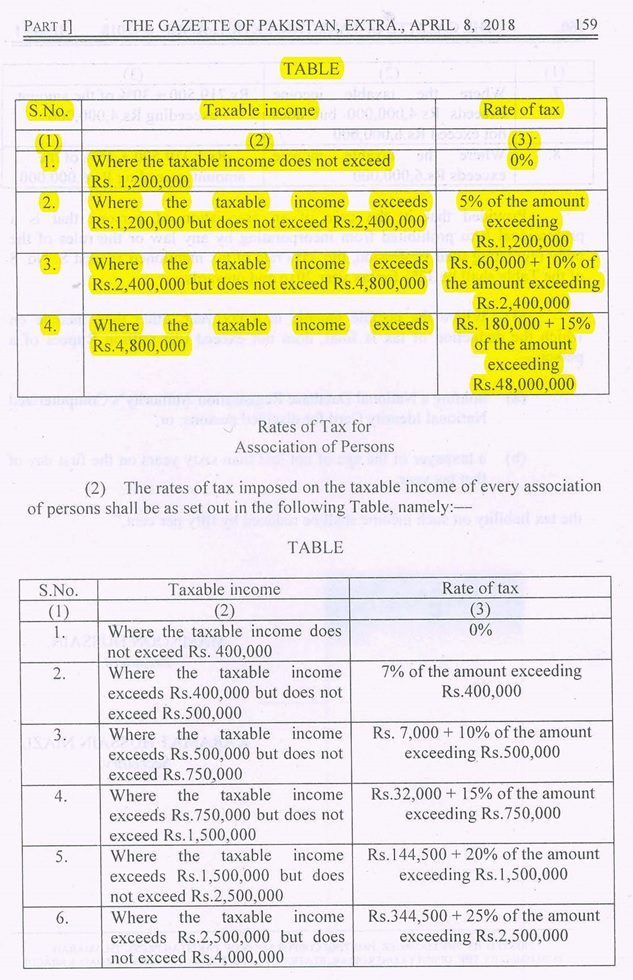

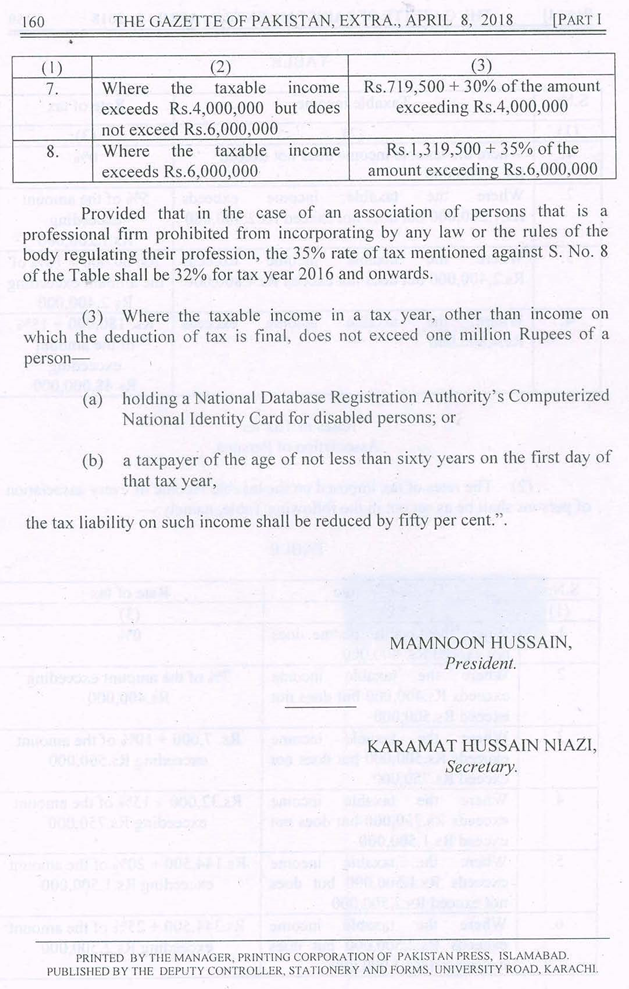

The above placed DIVISION-I of PART-I of SCHEDULE-I has now been replaced by newly laid Ordinance i.e. Income Tax (Amendment) Ordinance 2018:

From the above amendments, it can clearly be seen that DIVISION-I of PART-I of SCHEDULE-I of Income Tax Ordinance 2001 (Amended upto 30-06-2017) has now been changed with new DIVISION-I (As highlighted in yellow colour).

CONCLUSION:

Income Tax (Amendment) Ordinance, 2018 will be applied to all the individuals earning more than 100,000/- per month. Individuals earning less than 100,000/- per month will not be liable to Income Tax as per newly laid ordinance.

حال ہی میں انکم ٹیکس (امینڈمینٹ) آرڈیننس 2018 متعارف کروایا گیا ہے، جس میں انکم ٹیکس آرڈیننس2001 (تبدیلی از تاریخ 30جون2017) کو کچھ حد تک تبدیل کیا گیا ہے۔ اِس تبدیلی میں ملازمین کے لیے ایک بہت بڑا ریلیف مہیا کیا گیا ہے ۔ انکم ٹیکس (امینڈمینٹ) آرڈیننس 2018 میں شیڈول -1 میں موجود پارٹ-1میں موجود ڈویژن -1 میں مکمل طور پر تبدیلی گئی ہے اور اِس میں نئے اِنکم ٹیکس ریٹس وضع کیے گئے ہیں۔ یہاں یہ بات واضح کرنا ضروری ہے کہ پہلے جو انکم ٹیکس وصول کیا جاتا تھا، وہ شیڈول -1 میں موجود پارٹ-1میں موجود ڈویژن -1 کے مطابق لیا جاتا تھا ۔ اب شیڈول -1 میں موجود پارٹ-1میں موجود ڈویژن -1کو مکمل طور پر نئے آرڈیننس کے ذریعے تبدیل کر دیا گیا ہے۔ لہٰذا پہلے ریٹ پر لیا جانے والا انکم ٹیکس 30جون 2018کے بعد قابلِ عمل نہیں ہوگا۔

مزید معلومات کیلئے ای-میل کیجئے:

Download Income Tax (Amendment) Ordinance 2018

Can you provide any notification or signed copy of gazette ?

Thank you

Dear Adil welcome.