Last Updated on March 22, 2026 by Galaxy World

Government of Sindh, Finance Department issued a Notification on 21-08-2025 in connection with the Pension Contribution Scheme 2025 Sindh Civil Servants (Defined Contribution Pension) Rules 2025. The details are as follows:

Pension Contribution Scheme 2025 Sindh

GOVERNMENT OF SINDH FINANCE DEPARTMENT Karachi, dated 21 August 2025

NOTIFICATION NO.FD(SR-II1)3-2356/2024: In exercise of the powers conferred under section 26 of the Sindh Civil Servants Act, 1973 (XIV of 1973), Government of Sindh is pleased to make the following rules:-

-

Short title, commencement, and application

(1) These rules may be called the Sindh Civil Servants (Defined Contribution Pension) Rules, 2025.

(2) They shall come into force at once.

(3) They shall apply to all the employees mentioned in clause (j) of sub-rule (1) of rule 2 of these Rules.

-

Definitions:

(1) In these rules, unless the subject or context requires otherwise -(a) “Accountant General” means the Accountant General, Sindh; (b) “Act” means the Sindh Civil Servants Act, 1973 (Sindh Act No.XIV of 1973), as amended from time to time; (c) “allocation policy” means allocation of contributions in various sub-funds of an employer pension fund in accordance with these rules and governed by the Voluntary Pension System Rules, 2005 and the Non-Banking Finance Companies and Notified Entities Regulations, 2008; (d) “conventional fund” means a type of employer pension fund to be managed by the Eligible Pension Fund Manager, in a conventional manner, in accordance with the Voluntary Pension System Rules, 2005;

Defined Contribution Pension Scheme” means the Defined Contribution Pension cheme as specified in section 20 (1) of the Act and these rules and shall be governed accordance with the Voluntary Pension System Rules, 2005 and the Non-Banking inance Companies and Notified Entities Regulations, 2008, under which both the employer and employee contribute, as per the First Schedule, to the employee’s pension account, opened with an Eligible Pension Fund Manager of the employee’s choice, and such contributions are invested in an employer pension fund as defined under the Voluntary Pension System Rules, 2005, either in a conventional fund or a Shariah compliant fund, as selected by the employee, until the employee attains the retirement age, and the accumulated balance in the pension account at the time of retirement is withdrawn (to the extent allowable) or invested further to generate monthly income during the post-retirement phase, subject to exceptions under these rules;

(f) “Department” means a department as defined in the Sindh Government Rules of Business, 1986;

(g) District Accounts Officer” means an officer who carries out the work of accounting and is responsible for the compilation and consolidation of accounts of a District;

(h) Drawing and Disbursing Officer” means an officer responsible for drawing money from the Government Accounts Office and disbursing it on behalf of the Government to the claimant under these rules;

(i) Eligible Pension Fund Manager” means a Pension Fund Manager who qualifies the criteria as specified in sub-rule (16) of rule 4 and has entered into an agreement with the employer to establish and manage employer pension funds for the employees;

(j) “employee” means

(i) a person appointed on or after the commencement of the Sindh Civil Servants (Amendment) Act, 2024, but not including any person who was appointed as Government servant holding pensionable post before the commencement of the said Act, and was subsequently inducted into any Provincial Civil service through proper channel after coming into force of the Sindh Civil Servants (Amendment) Act, 2024; or

(ii) a person regularized as a civil servant through any legal instrument issued on or after the commencement of the Sindh Civil Servants (Amendment) Act, 2024, and shall be considered an employee for the purposes of these rules from the date of issuance of such legal instrument, regardless of the effective date of regularization:

Provided that an employee shall, subject to sub-rule (3) of rule 5 of these rules, be deemed to be an employee solely for the purposes of the Defined Contribution Pension Scheme until reaching the retirement age and no further contributions shall be made to his pension account by either the employer or the employee in the event of his leaving service before attaining the retirement age for any reason whatsoever;

(k) “employer” means the Government of Sindh;

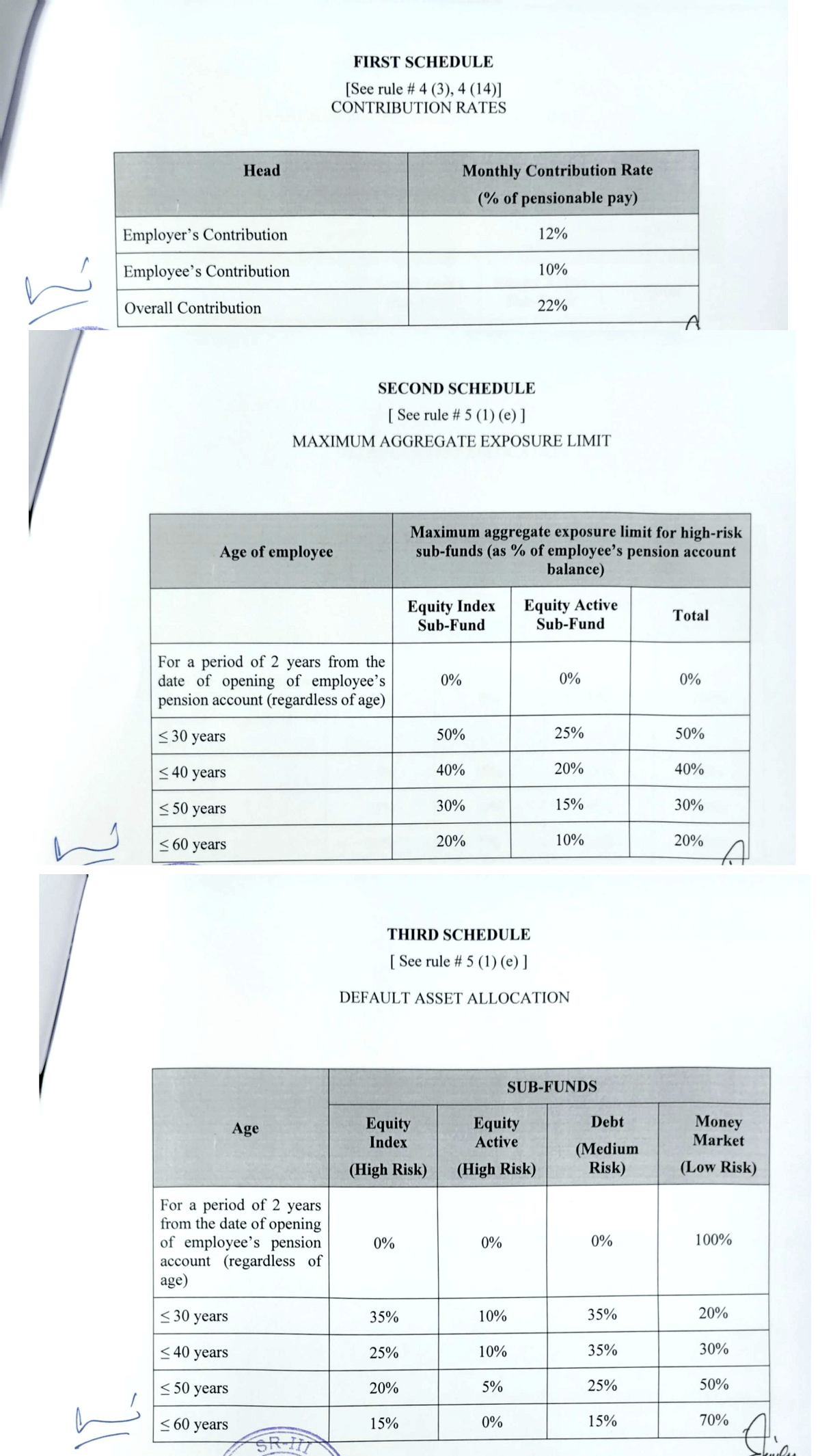

(l) “employee’s contribution” means the amount, computed by multiplying the employee’s pensionable pay by the employee’s contribution rate, as specified in the First Schedule;

(m) employer’s contribution” means the amount, computed by multiplying the employee’s pensionable pay by the employer’s contribution rate, as specified in the First Schedule;

(n) “Finance Department” means the Finance Department, Government of Sindh;

(o) Government” means the Government of Sindh;

(p) “overall contribution” means the sum of the employer’s contribution and the employee’s contribution as per the First Schedule;

(q) “overall contribution rate” means the sum of the employer’s contribution rate and the employee’s contribution rate as specified in the First Schedule;

(r) “pension account” means an account opened and maintained by an employee with the Eligible Pension Fund Manager in accordance with the Voluntary Pension System Rules, 2005;

(s) “Pension Fund Manager Agreement” means an agreement between the employer and the Eligible Pension Fund Manager for the Defined Contribution Pension Scheme;

(t) “pensionable pay” means the running basic pay, including personal pay, but does not include any other pay, allowances, or perquisites;

(u) “retirement age” means the age as specified in section 13 (1) (ii) (a) of the Act;

(v) “Voluntary Pension System Rules, 2005” means the rules issued by the Securities and Exchange Commission of Pakistan (SECP) governing the Voluntary Pension System, as amended from time to time; (w) “salary” means the monthly amount being drawn as pay and allowances by the employee;

(x) “Schedule” means the Schedule appended to these rules;

(y) “Self-Accounting Entity” means any accounting entity for which the Principal Accounting Officer has primary responsibility for the accounting and reporting functions;

(z) “Shariah compliant fund” means a type of employer pension fund, governed by the requirements of Shariah law to be managed by the Eligible Pension Fund Manager in accordance with the Voluntary Pension System Rules, 2005;

(aa) “Unit” means the Sindh Contribution Pension Unit established under these rules.

(2) The words or expressions used but not defined in these rules shall have the same meaning as assigned to them in the Act and the Voluntary Pension System Rules, 2005.

3. Governance of the Defined Contribution Pension Scheme. (1) Save as otherwise provided in these rules, the Defined Contribution Pension Scheme shall be governed in accordance with the Voluntary Pension System Rules, 2005, and the Non-Banking Finance Companies and Notified Entities Regulations, 2008.

(2) The Defined Contribution Pension Scheme shall be managed through the Eligible

ion Fund Managers.

(3) The balance in the pension account, including the employer’s contribution and yee’s contribution, and the return thereon, shall be subject to these rules. Role and responsibilities of the employer.

(1) The Department shall ensure that the employer’s contribution is made and the employee’s contribution is deducted at source at the time of each salary payment, through the Accountant General of Sindh.

(2) The employer’s contribution, being part of the overall contribution under the Defined Contribution Pension Scheme, shall be made in addition to the salary otherwise payable to the employee:

Provided that, in the case of an employee on deputation outside the Government, the liability for payment of the employer’s contribution during the period of deputation shall be determined in accordance with the terms and conditions governing such deputation, as agreed between the borrowing entity and the employer.

(3) The employer shall not be under any obligation to make any additional contribution or payment for the Defined Contribution Pension Scheme in addition to the rates as mentioned in the First Schedule.

(4) The employer shall ensure budgetary allocations for its contribution, and the Finance Department shall release funds in a timely manner without any exception.

(5) All Departments shall submit budgetary requisitions to the Finance Department for the allocation of funds necessary to make the employer’s contribution under the Scheme.

(6) The Accountant General shall transfer the overall contribution in the employee’s pension account at the time of payment of salary to the employee through an automated system implemented and managed by him without any delay.

(7) The Accountant General shall be responsible for the deduction, transfer, accounting, and reconciliation of both the employer’s contribution and the employee’s contribution.

(8) The Accountant General shall forward monthly reports to the Unit regarding the transfer of contributions in accordance with the agreed-upon reporting format and timelines.

(9) In cases where an employee’s salary is disbursed by a self-accounting entity owned or controlled by Government, instead of through the Accountant General or the District Accounts Officer, as the case may be, the Drawing and Disbursing Officer of such entity shall transfer the overall contribution to the respective pension account of the employee at the time of salary disbursement with the intimation to the Unit. This arrangement shall continue until the salary of the said employee begins to be disbursed through the Accountant General or the District Accounts Officer, as applicable. The self-accounting entity shall be solely responsible for the employer’s contribution. The Drawing and Disbursing Officer shall maintain complete and accurate records of monthly contributions and transfers made in accordance with these rules, in the manner prescribed by the Unit.

Provided that, in the event of any delay in transferring the overall contribution, the Drawing and Disbursing Officer shall be liable to compensate the employee by making an additional contribution into the employee’s pension account, equivalent to the profit or gain as the employee would have earned or realized had the overall contribution en transferred in a timely manner. The amount of such additional contribution shall be determined by the Unit.

(10) The Accountant General or District Accounts Officer, as the case may be, shall process the first salary of an employee, subject to the completion of requirements mentioned in sub-rule (16), (20) and (21) (b) of rule 4 and after receiving the information regarding his pension account as per clause (b) of sub-rule (1) of rule 5 of these rules.

Explanation:-

“First Salary” in this rule shall mean the salary that shall be disbursed after a person becomes an employee.

(11) The Drawing and Disbursing Officer shall obtain the particulars of the employee’s pension account from the employee and submit the same to the Accountant General or District Accounts Officer, as the case may be, in the manner as the Accountant General or District Accounts Officer may prescribe. The Accountant General or District Accounts Officer, as the case may be, shall, upon receipt of such particulars, ensure that they are duly recorded and updated in the system, as and when required.

Explanation:-

For the purposes of this sub-rule, the manner of submission shall be as prescribed by the Accountant General or District Accounts Officer, as the case may be.

(12) The salary slip of each employee shall include information regarding the employee’s and employer’s contributions transferred in the said month’s salary, as well as accumulated employee’s and employer’s contributions to date:

Provided that, where the salary is disbursed by a self-accounting entity owned or controlled by the Government other than the Accountant General or District Accounts Officer, as the case may be, the Drawing and Disbursing Officer concerned shall ensure the inclusion of this information on the salary slip, based on records maintained in accordance with these rules.

(13) The Drawing and Disbursing Officer, in case where salary of an employee is disbursed by a self-accounting entity owned or controlled by the Government other than the Accountant General, as the case may be, shall compute and deduct income tax from the employee’s salary in accordance with the provisions of the Income Tax Ordinance, 2001 (XLIX of 2001), and also adjust the employee’s monthly tax deductions to reflect any rebate available under the said Ordinance in respect of contributions to the Voluntary Pension System Rules 2005.

(14) The Drawing Disbursing Officer, in cases where the salary of an employee is disbursed by a self-accounting entity owned or controlled by the Government, shall not deduct and transfer the overall contribution for any employee whose pension account has not been opened. On opening of his pension account, any outstanding overall contributions for the period commencing from the date he becomes an employee till the date of opening of his pension account shall be deducted and transferred to his pension account in future months, in addition to the regular overall contributions, in accordance with the First Schedule:

Provided that such additional overall contribution shall not be more than the regular overall contribution until all outstanding overall contributions are accounted for:

Provided further that the Drawing and Disbursing Officer shall obtain prior budget allocation for the employer’s share of such contributions and convey to the Accountant General or District Accounts Officer, as the case may be, where the salary is disbursed through the Accountant General or District Accounts Officer, as the case may be, or retained in the cost center of the concerned self-accounting entity, where the salary is disbursed by a self-accounting entity owned or controlled by Government other than the Accountant General or District Accounts Officer, as the case may be. No such deductions shall be made until the requisite budget has been placed in the relevant cost centre and the Unit under the Finance Department has been duly informed.

(15) The Accountant General or District Accounts Officer, as the case may be, shall identify and rectify any omission or error in the deduction of the employee’s contribution and the employer’s contribution, or both, irrespective of the underlying cause. Where salary has been paid without the required deductions, or where the deducted amounts are incorrect, the concerned Drawing and Disbursing Officer shall promptly report the omission or error to the Accountant General or District Accounts Officer, as the case may be, in the format and manner prescribed by the Accountant General or District Accounts Officer, as the case may be, and shall submit the necessary payroll adjustments for the relevant period. The Accountant General shall also conduct independent monthly payroll reconciliations to identify such omissions or errors. Upon identification, whether through reconciliation or reporting by the Drawing and Disbursing Officer, the Accountant General Accountant General or District Accounts Officer, as the case may be, shall recover any outstanding contributions, or adjust the amount to be ectified, in future salary cycles, in addition to the regular monthly contributions, subject to the imit specified in sub-rule (14) of rule 4.

(16) The employer, through the Finance Department, shall enter into the Pension Manager Agreement with each of the Pension Fund Managers who.

(a) is authorized under the Voluntary Pension System Rules, 2005 to manage employer pension funds; (b) meets the asset manager rating criteria specified in the Voluntary Pension System Rules, 2005;

(c) has systems that support electronic transfer of contributions; and

(d) has applied to the Government to provide services for managing pension fund(s) for its employees in accordance with these rules and the Voluntary Pension System Rules, 2005.

(17) The Pension Fund Manager Agreement shall specify the standard terms and conditions, including a mandatory insurance plan providing death and disability risk cover to the employees to be arranged by the Eligible Pension Fund Manager in accordance with the Pension Fund Manager Agreement.

(18) The Finance Department shall notify a list of Eligible Pension Fund Managers and publish it on its website, and keep the same updated.

(19) The employer may, through the Finance Department, terminate the Pension Fund Manager Agreement with the Eligible Pension Fund Manager in accordance with the terms and conditions as specified in the Pension Fund Manager Agreement.

(20) The Finance Department shall ensure that each Eligible Pension Fund Manager establishes separate pension fund(s) for the Defined Contribution Pension Scheme, and each pension fund shall include the sub-funds as specified by the Finance Department, from time to time.

(21) The Finance Department shall establish the Sindh Contribution Pension Unit, which.

(a) Monitor the Defined Contribution Pension Scheme;

b) establish and maintain an online portal to facilitate the smooth opening of pension accounts and the ongoing monitoring of the Defined Contribution Pension Scheme, providing a user-friendly interface for employees to open their pension accounts and communicate with the Unit and enabling real-time data sharing between the Unit, the Eligible Pension Fund Managers and other relevant entities to ensure transparency efficiency and effective management of the Defined Contribution Pension Scheme;

(c) require and analyze periodic reports from the Eligible Pension Fund Managers, including but not limited to information regarding —

(i) number of pension accounts;

(ii) number of pension account holders;

(iii) amount of contributions received;

(iv) performance of sub-funds of the pension funds being managed;

(v) pension account holders who have reached the retirement age and the amount withdrawn by such pension account holder; and

(vi) number of employees who have invested in monthly income plans and annuities, and the amount of monthly profit and annuity paid to such employees;

(d) prepare and disseminate training materials for the education of the employees regarding:

(i) these rules and the Voluntary Pension System Rules, 2005;

(ii) selection from among the Eligible Pension Fund Managers;

(iii) opening of pension account;

(iv) setting up online access to the pension account;

(v) choosing or revising allocation policy;

(vi) understanding account statements;

(vii) updating any changes in personal information; and

(viii) transferring pension account from one Eligible Pension Fund Manager to another, etc.;

(e) provide separate updated lists to the Eligible Pension Fund Managers in respect of the employees;

(i) whose pension accounts are to be opened; or

(ii) who have left employment before attaining the retirement age; or

(iii) who have attained the retirement age;

(iv) who have died before or after attaining the retirement age;

(f) act as an intermediary between the employees and Eligible Pension Fund Managers for opening of pension accounts and performing necessary tasks in this respect, including obtaining the information required for opening of pension account from the employees according to the template jointly developed by the Eligible Pension Fund Managers, sharing the information with Eligible Pension Fund Managers, resolving any discrepancies or deficiencies and ensuring that the pension accounts are opened as soon as practicable; ensure that only one designated pension account is recorded for each employee with the Accountant General or District Accounts Officer, as the case may be, in cases where the salary is disbursed through the Accountant General Accountant General or District Accounts Officer, as the case may be;

(g) and with the self-accounting entity, in cases where the salary is disbursed by a self-accounting entity owned or controlled by the Government of Sindh other than the Accountant General, or District Accounts Officer, as the case may be;

(h) facilitate the employees in resolution of any issue such as updating of personal information, using online services, understanding their account statements and notifying the pension account holder about the termination or cancellation of the Pension Fund Manager Agreement with an Eligible Pension Fund Manager by the employer; coordinate with relevant stakeholders for resolving any issue that may arise in connection with the Defined Contribution Pension Scheme;

(b) provide the relevant information regarding his pension account, including his selection between a conventional fund or a Shariah compliant fund, to the Accountant General or District Accounts Officer, as the case may be, through the concerned Drawing and Disbursing Officer on such forms as specified by the Accountant General for this purpose: Provided that, in cases where an employee’s salary is disbursed by a self-accounting entity owned or controlled by Government, instead of through the Accountant General or the District Accounts Officer, as the case may be, the employee shall provide such information to, and have it recorded with, the Drawing and Disbursing Officer of that entity;

(c) make his contribution from his salary in accordance with these rules;

(d) be entitled to his pension account balance from the date of qualifying for the Defined Contribution Pension Scheme in accordance with these rules and subject to the conditions as specified in the Voluntary Pension System Rules, 2005;

(e) determine the allocation policy for the contributions in his pension account among the sub-funds of the employer pension fund, subject to the exposure limits as specified in the Second Schedule, and shall communicate the allocation policy and any changes therein to the Eligible Pension Fund Manager through the Unit;

Provided that an employee who does not indicate his allocation policy, his pension account shall be managed in accordance with the default allocation policy as specified in the Third Schedule;

have the option to transfer his pension account with a particular Eligible Pension Fund Manager to another Eligible Pension Fund Manager in accordance with the Voluntary Pension System Rules, 2005, and

not withdraw any amount from his pension account before attaining the retirement age.

(2) Upon attaining the retirement age, the employee may withdraw in lump sum not more than twenty five percent (25%) of the accumulated balance in his pension account and shall invest the remaining balance in accordance with the Voluntary Pension System Rules, 2005, for a period of at least twenty years (20) or till his death, whichever is earlier.

(3) Notwithstanding any other provision of these rules, where an employee either resigns, retires voluntarily, or otherwise quits service, or where the service of an employee is discontinued by employer for any reason whatsoever, in each case prior to attaining the retirement age, the employee may, by informing the Unit in writing, opt to no longer be subject to these rules and transfer his pension account from the employer pension fund to another employer pension fund or withdraw the accumulated balance in his pension account subject to the Voluntary Pension System Rules, 2005 and other applicable laws. (4) In the event of pecuniary loss to the Provincial exchequer resulting from an employee’s action, omission or negligence, such employee shall be personally liable to make good such loss in the manner as provided under the Sindh Civil Servants (Efficiency & Discipline) Rules, 1973 and such liability shall extend to losses discovered after the employee’s retirement or discontinuation from service or death in accordance with the provisions of relevant law and rules in force.

- Precedence over the other rules. These rules shall have precedence over any other rules, for the time being in force, if any inconsistency arises between these rules and the other rules.

Post Schedule

(see Rule No 4 (3), 4 (14))

Contribution Rates

| Sr | Head | Monthly Contribution Rate (% of pensionable pay) |

| 1 | Employer’s Contribution | 12% |

| 2 | Employee’s Contribution | 10% |

| 3 | Overall Contribution | 22% |

| Sr No | Age of e,ployee | Maximum aggregate exposure limit for high-risk sub-funds as % of employee’s personal account balance) | ||

| For a period of 2 years from the date of opening of the employee’s pension account (regardless of age) | Equity Index Sub-Fund | Reuity Active Sub-Fund | Total | |

| 0% | 0% | 0% | ||

| 1 | < 30 years – |

50% | 25% | 50% |

| 2 | < 40 years – |

40% | 20% | 40% |

| 3 | < 50 years – |

30% | 15% | 30% |

| 4 | < 60 years – |

20% | 10% | 20% |

Third Schedule (see Rule no 5 (1) (e) )

Default Asset Allocation

| Sr No | Age | Sub-Funds | |||

| For a period of 2 years from the date of opening of the employee’s pension account (regardless of age) | Equity Index (High Risk) | Equity Active (high Risk) | Debt (Medium Risk) | Money Market (low Risk) | |

| 0% | 0% | 0% | 100% | ||

| 1 | < 30 years – |

35% | 10% | 35% | 20% |

| 2 | < 40 years – |

25% | 10% | 35% | 30% |

| 3 | < 50 years – |

20% | 5% | 25% | 50% |

| 4 | < 60 years – |

15% | 0% | 15% | 70% |

Download Notification Sindh Civil Servants (Defined Contribution Pension) Rules 2025 Year

You may also like: Notification of Reduction Factor on Voluntary Retirement Sindh 2025

AoA,

If someone was regular employee and worked for ten years

Then he joins a contractual higher post and subsequently regularise through regularisation act 2018 recently in 2025.

1. Please guide whether he will be the subscriber of defined contributory pension scheme or Not.

2. Secondly, I know that the increments earned on contractual post will not be protected and the increments earned, will be given as Personal Allowance

Please guide the protection of his substantial pay of his substantive post?

I shall confirm the same situation soon IA.